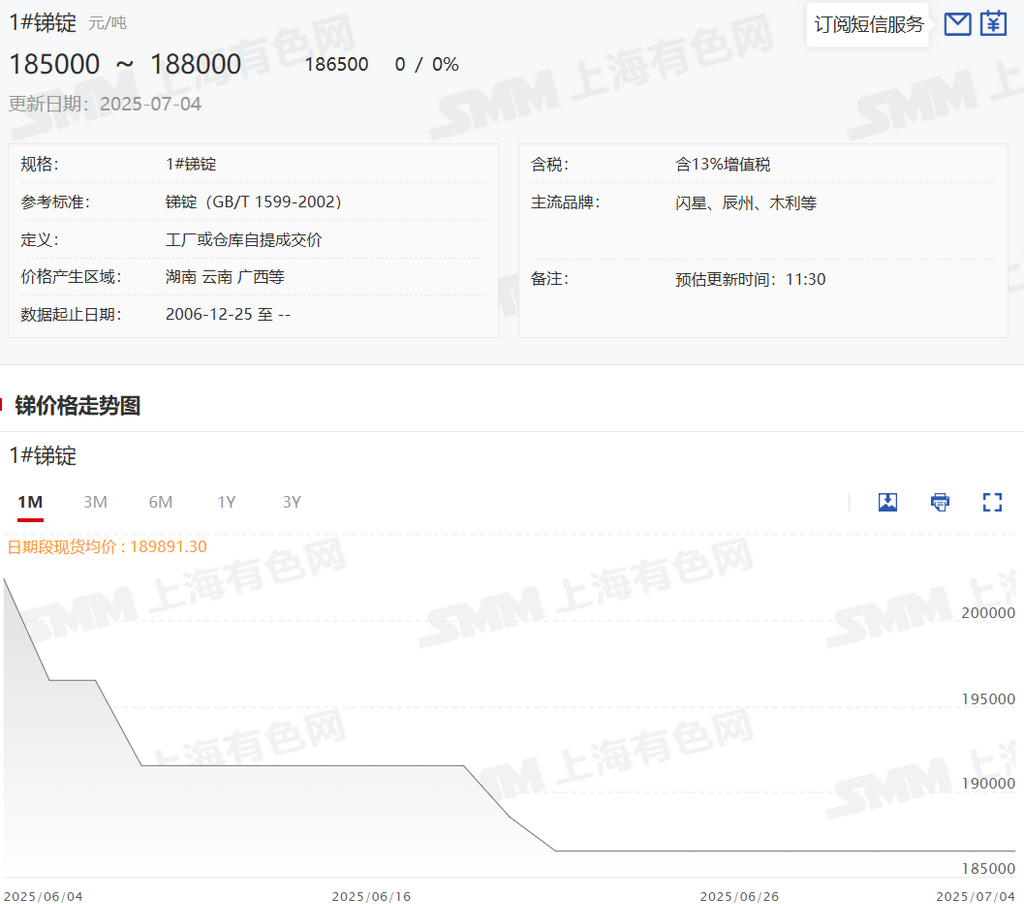

SMM July 4: Antimony prices remained stable this week, showing signs of bottoming out and transitioning to a stronger trend. Many market participants believe that, in terms of supply, tight raw material supply has led to insufficient production, with manufacturers' finished product inventories remaining low. Similarly, downstream players currently hold almost no raw material inventories. As antimony prices stabilize, downstream concerns about potential volatile market conditions may prompt stockpiling preparations at any time. Once downstream stockpiling begins, speculative capital is likely to follow, making the current antimony price trend worth monitoring. As of now, SMM's average antimony prices stand at: No.2 low-bismuth ingot at 180,500 yuan/mt, No.1 ingot at 186,500 yuan/mt, No.0 ingot at 190,500 yuan/mt, and No.2 high-bismuth ingot at 177,500 yuan/mt. For antimony trioxide, the average prices are: 99.5% grade at 160,500 yuan/mt and 99.8% grade at 172,500 yuan/mt.

According to SMM estimates, China's antimony ingot production (including ingots, crude antimony conversion, antimony cathode, etc.) in June 2025 decreased sharply by approximately 21.5% MoM. Specifically, among the 33 surveyed entities, 15 producers reported zero output (up 4 MoM), 15 showed production cuts (down 4 MoM), and 3 maintained normal production levels (unchanged MoM). Following a slight production increase in May, June saw another significant decline, which many market participants consider normal. Recent sharp price drops have increased production elasticity, while summer maintenance shutdowns have forced many producers to limit output, reduce inventories, and ease sales pressure. Imported ore supply remains constrained, keeping domestic raw material supply tight. More production cuts are expected to be announced from late June to early July. Market participants anticipate China's antimony ingot production in July 2025 will likely continue declining compared to June.

SMM estimates show China's sodium pyroantimonate (first-grade) production in June 2025 increased approximately 13.23% MoM. After months of volatility and a May decline, June's rebound surprised many market participants. However, this is considered normal due to the PV installation rush from May to June and increased glass factory orders ahead of the overseas summer break starting late June. Many producers attributed their June output growth to additional orders, though it remains uncertain whether this trend will continue into July. Looking at the detailed data, among SMM's 13 survey respondents, 4 manufacturers were in a state of shutdown or commissioning in June. The production of 4 sodium pyroantimonate manufacturers increased, but 1 manufacturer also experienced a decline in production. As a result, the overall production of first-grade sodium pyroantimonate in China increased significantly in June. Market participants expect that the possibility of a continued significant increase in nationwide sodium pyroantimonate production in July compared to June is relatively small, and it is more likely to remain stable or increase slightly.